Fidelity Retirement Planner

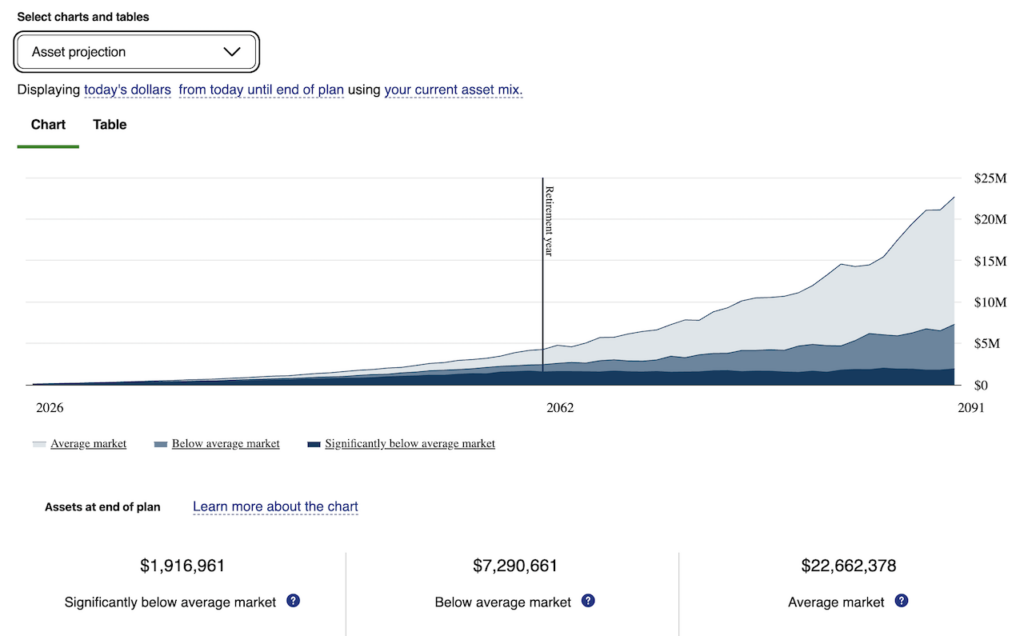

Fidelity is one of the largest brokerage companies in the world offering financial services including free online financial planning tools. The Fidelity Retirement Planning dashboard allows users to create a personal household profile (income, bonus, commission), retirement profile (retirement age, state, life expectancy), retirement expenses (can use automatic estimate or define user input), current assets (401k, saving, investment, real estate) and retirement income (social security, can use automatic estimate or manual input). The result from the analysis is a basic graph showing projection for 3 different scenarios, average market, below average market and significantly below average market.

The tool is very simple and easy to use. If the user already has a Fidelity account for 401k or IRA, all of these assets are automatically linked to the tool to be used in the analysis. These types of accounts can also be added manually. The user also has option to manually add in other assets. The analysis result is very easy to interpret and can be viewed with a graph or a table showing the growth of the total assets through each year until the final year of life expectancy.

Some of the limitations of the tool is that it does not offer different rate of return assumption. Retirement saving rate is set to the user’s current 401k contribution rate and cannot be adjusted easily, which limits the user’s ability to see what happens if they decide to save more or less. It is not clear how the tool takes into account the user’s current expenses and how that factors into their saving plan and retirement projection.

Empower

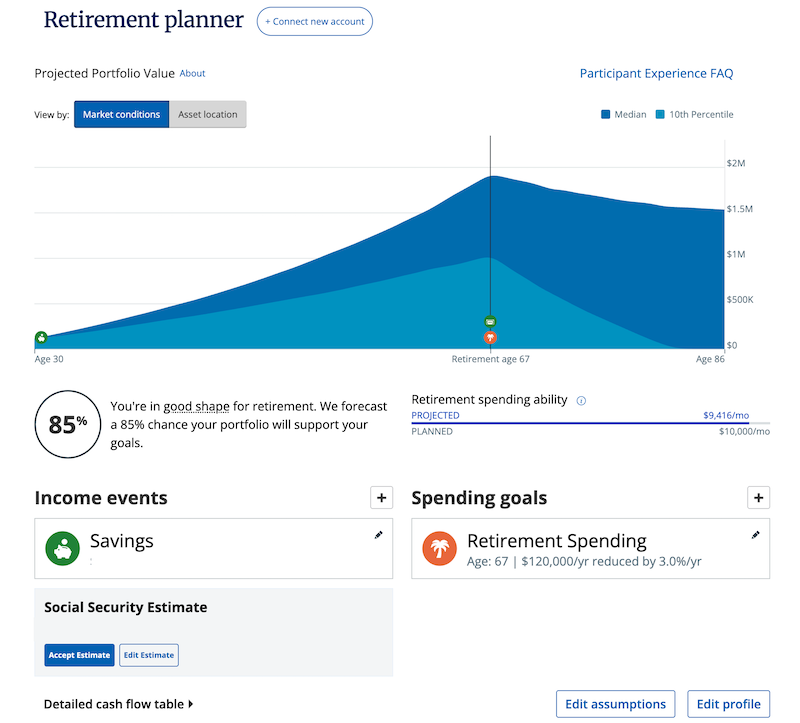

Empower is another financial services company providing free financial planning tool that allows users to track finances, budgeting and retirement planning. The tool requires setting up an Empower account and link all personal information such as bank accounts, retirement accounts, mortgage, loans, etc. In the retirement planner, the user can input their expected yearly saving, any other cash balance and a percentage of saving increase per year. The user can also adjust retirement age, retirement spending and percentage of spending decrease per year until reaching a spending minimum. There is also a social security estimate provided by the software but can be manually adjusted by the user. There are a few assumptions that the user can manipulate such as effective tax rate, inflation rate and life expectancy. The analysis result shows a graph of the projected portfolio over the projected lifespan with a success rate given in percentage.

One drawback of the tool is that it requires the user to link personal financial accounts, which might be viewed as a security concern. It also has limited capability in term of making adjustment to saving plan or adding a spouse to the profile. Similar to Fidelity Retirement Planning, this tool assumes a fixed saving rate and does not take into account monthly expenses and how variations might factor into retirement projection.

On the other hand, one advantage of the tool is that it allows the user to create multiple retirement plans, simulate recession at a certain year during the user’s lifetime, compare these different scenarios and evaluate the rate of success for each plan. Overall, the tool has a very user-friendly interface with an easy learning curve suitable for beginners looking into retirement planning.

ProjectionLab

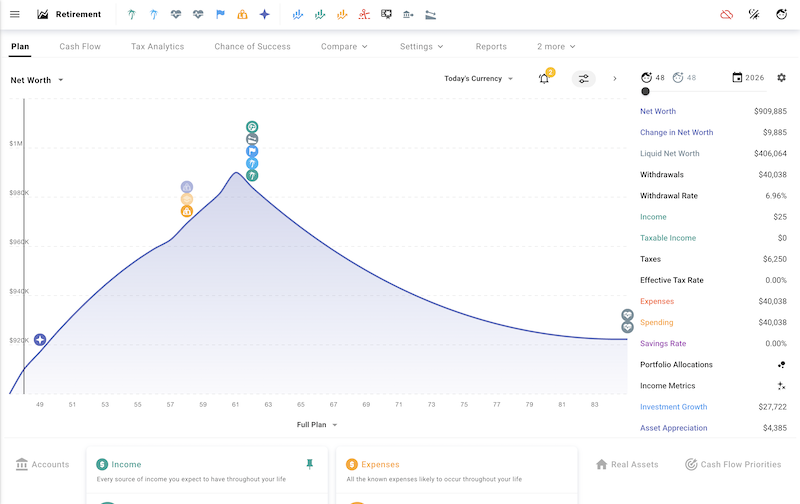

ProjectionLab Financial Planning tool has a free version as well as premium for advanced users. The free version offers full planning capabilities, but some advanced reporting is limited to premium members only. Aside from the basics, this tool has an option to add life milestones such as getting married, having kids, new jobs or moving to a different place. The user can also input current living expenses and cash flow priorities such as paying debt and mortgage.

The tool requires the user to manually input all of their information. However, there is no data preservation in the free version, and the user would have to manually input all the numbers again at their next visit. The tool utilizes Monte Carlo probability analysis to simulate the chance of success in reaching retirement goal. A huge drawback of the tool is that it has a high learning curve due to the level of customization and complexity in trying to simulate real life scenarios.

Start your retirement planning journey today